FOMC Transcripts as Onchain Trading Strategy Inputs: A Backtest Walkthrough

Learn how to turn FOMC text into an onchain trading strategy research input without lookahead bias, then test it before using live macro alerts.

Short answer

FOMC text can be useful in onchain trading strategy research, but the data source matters.

Meeting transcripts are historical research material, not a live trading feed. They are released long after the meeting, so using them as if they were available on event day creates lookahead bias. For live workflows, use scheduled FOMC events and same-day public materials such as statements, press conferences, market reaction, and manually verified summaries.

The right workflow is to turn the macro thesis into a rule, separate research labels from live inputs, backtest the condition, and start with alerts.

Why FOMC events matter for onchain markets

Onchain markets trade 24/7, and crypto is the clearest live surface today, but they still react to dollar liquidity, rates expectations, risk appetite, and leverage conditions. FOMC days can change all four at once.

That does not mean every meeting creates a tradable edge. It means event context should be explicit when testing an onchain market rule:

- Is the rule allowed to fire before the FOMC decision?

- Does it behave differently after the statement?

- Does a hawkish or dovish read change forward returns?

- Is the signal only working because one volatile event dominates the backtest?

If those questions are not modeled, the strategy can look cleaner than it really is.

Transcripts, minutes, statements, and live data are different

Do not put every Fed document into one bucket.

| Source | Practical use | Risk | | --- | --- | --- | | FOMC calendar | Live event timing | Tells you timing, not sentiment | | Statement | Same-day event text | Needs fast interpretation and market context | | Press conference | Same-day qualitative context | Noisy and easy to overfit | | Minutes | Delayed meeting detail | Not available during the meeting | | Transcript | Historical research label | Lookahead bias if treated as live input |

The transcript is useful for studying what policymakers discussed, but it should not be used as if a trader had it during the event. In a backtest, treat it as a later label or analysis layer unless your strategy explicitly waits for release.

Define the macro feature

A usable FOMC feature should be simple enough to test:

- Event window: 2 hours before decision through 4 hours after press conference.

- Tone label: hawkish, dovish, or neutral.

- Market reaction: BTC return, dollar move, rates move, or volatility change after release.

- Avoidance rule: do not fire during the event window.

- Regime split: compare FOMC days with non-FOMC days.

Start with one feature. A rule with ten macro labels will probably fit the past better than it works live.

Example prompt

Use a prompt that separates live inputs from research labels:

Backtest BTC-PERP on Hyperliquid. Signal when 8-hour funding is above 0.08% and price fails to make a new 4-hour high. Split results by FOMC event windows versus quiet days. For historical analysis, label FOMC events as hawkish, dovish, or neutral using public post-event materials, but do not let transcript labels enter the signal before their release date. Use a 4-hour cooldown and show 1-hour, 4-hour, and 24-hour forward returns.

That prompt gives the backtest engine the important boundaries:

- The base market signal.

- The FOMC event window.

- The quiet-day comparison.

- The transcript lookahead restriction.

- The cooldown and review horizons.

The output should show whether the base strategy behaves differently around macro events, not just whether a story sounds convincing.

Avoid lookahead bias

Lookahead bias happens when a backtest uses information that was not available at the time.

FOMC content creates several traps:

- Using transcript language to trade the original meeting day.

- Labeling a meeting with later analyst consensus and pretending the label was known live.

- Testing only famous events and ignoring quiet meetings.

- Choosing the event window after looking at the price chart.

- Mixing delayed minutes with same-day statement text.

The fix is procedural. For every input, write down when it became available. If the strategy could not have known it, it cannot be part of the live signal.

Backtest structure

A clean FOMC-aware onchain market backtest should include:

| Step | What to define | | --- | --- | | Base rule | Funding, price, OI, whale, or momentum condition | | Event calendar | Exact FOMC decision and press conference times | | Data availability | Which text was known at each timestamp | | Event handling | Avoid, include, or split results | | Cooldown | Minimum time between duplicate fires | | Review windows | 1h, 4h, 24h, or longer | | Baseline | Same rule on non-event days |

If the event version only works because it fired once during a historic move, treat that as a case study, not a strategy.

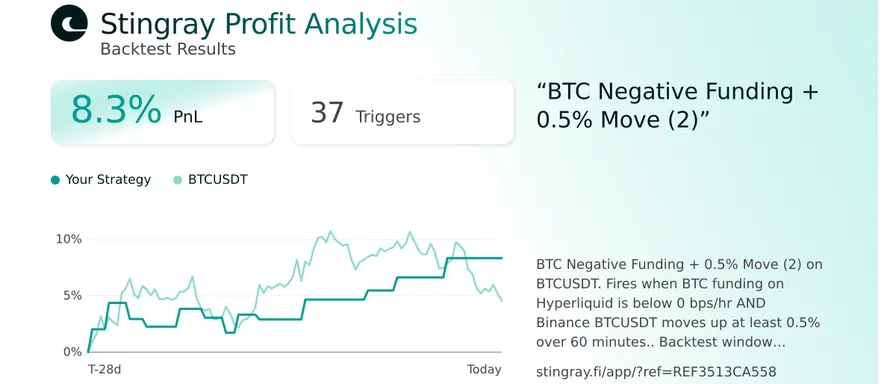

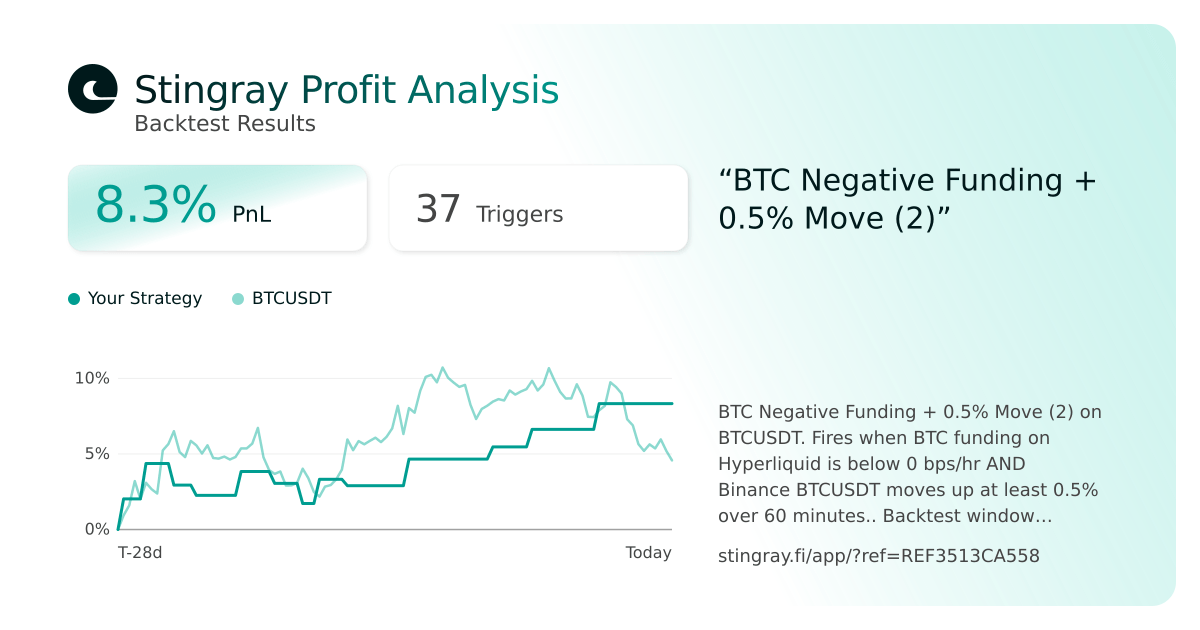

Where Stingray fits

Stingray is useful for turning the thesis into an inspectable rule before live risk: define the market condition, define the macro-event handling, backtest the exact trigger history, and then monitor the same rule as an alert.

If macro coverage is not available in your current workflow, keep the FOMC piece as a manual calendar filter and still test the onchain-native part of the strategy.

For related workflows, read How to Backtest a Strategy with Funding Rates and Macro Events, How to Automate a Funding Rate Strategy on Hyperliquid, and Whale Feed Strategies: How to Trade Open Interest Divergence.

Verdict

FOMC text can improve onchain market research only if the timing is honest.

Use statements, calendars, and verified same-day context for live workflows. Use transcripts as delayed research labels. Backtest event windows against quiet days, inspect every trigger, and start with alerts before moving toward execution.